![]()

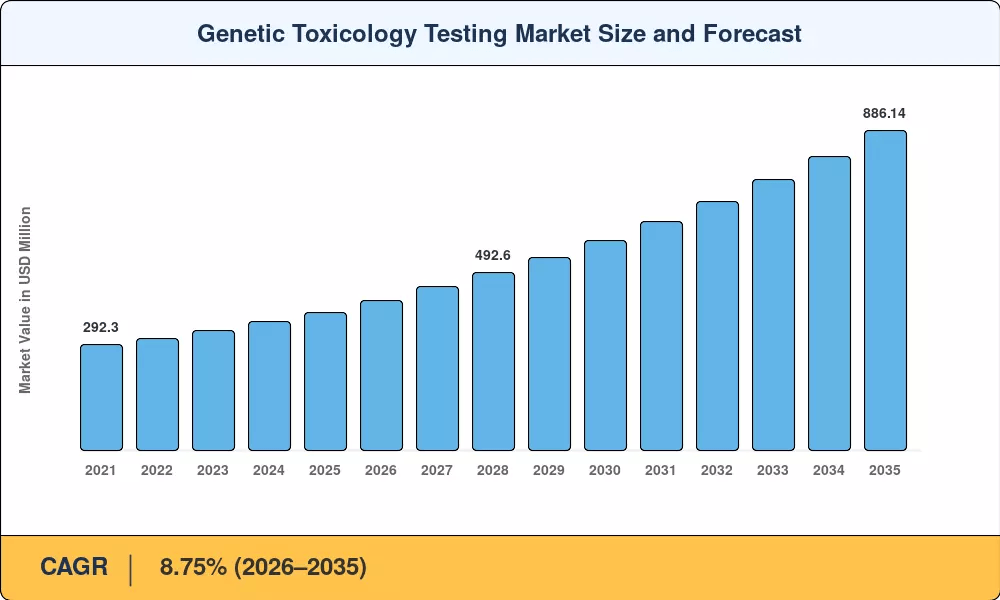

Genetic Toxicology Testing Market to Surge from $416.52 Mn in 2026 to $886.14 Mn by 2035-By FDA Modernization Act 2.0, Oncology & Biologics Pipeline

NY, CA, UNITED STATES, June 25, 2026 /EINPresswire.com/ — As per Market Research Future, the global Genetic Toxicology Testing Market size to reach USD 886.14 Million by 2035 from USD 416.52 Million in 2026, at a CAGR of 8.75% during the forecast period 2026–2035. The market base was estimated at USD 383.10 Million in 2025.

The 8.75% CAGR—anchored by regulatory mandates rather than discretionary healthcare spending—is driven by three converging forces: the FDA Modernization Act 2.0 and REACH revision eliminating statutory animal-testing language and channeling demand toward validated in vitro and computational genotoxicity assessment tools; the rapid scale-up of oncology and biologics pipelines—with global pharmaceutical R&D expenditure exceeding USD 288 billion in 2024 and over 6,500 molecules in active clinical development—requiring rigorous mutagenicity testing assays at every preclinical gate; and the technological shift from legacy rodent-based chromosomal aberration testing protocols toward 3-D spheroid cultures, organ-on-chip devices, and transformer-based predictive models that cut study cycle time by up to 40%.

Request A Free Sample:

https://www.marketresearchfuture.com/sample_request/32035

Key Market Trends & Growth Drivers

Regulatory Transition to Non-Animal Genotoxicity Assessment Tools and FDA Modernization Act 2.0

The FDA Modernization Act 2.0, signed in December 2022, struck mandatory animal-testing language from the Federal Food, Drug, and Cosmetic Act, opening a statutory pathway for sponsors to file INDs supported entirely by in vitro genotoxicity screening and computational evidence. Within 18 months, the agency approved three New Drug Applications that relied on integrated in silico/in vitro mutagenicity testing assays in place of traditional rodent studies, setting a precedent that European regulators are expected to mirror under REACH’s 2027 revision.

Oncology and Biologics Pipeline Intensification and Preclinical Safety Mandates

Global pharmaceutical R&D expenditure exceeded USD 288 billion in 2024, with oncology and biologics pipelines requiring rigorous mutagenicity testing assays at every preclinical gate. Global oncology R&D spending topped USD 68 billion in 2024, with over 6,500 molecules in active clinical development. Each candidate must pass a tiered battery of DNA damage testing services—starting with the Ames test genetic toxicology screen and advancing to chromosomal aberration testing and in vivo comet assays—before receiving first-in-human clearance.

3-D Cell-Culture, Organ-on-Chip Platforms, and AI-Enabled Predictive Toxicology Reshaping Testing Paradigms

Legacy rodent-based chromosomal aberration testing protocols and conventional Ames test genetic toxicology workflows are giving way to 3-D spheroid cultures, organ-on-chip devices, and transformer-based predictive models that cut study cycle time by up to 40%. Organ-on-chip devices developed by firms such as Emulate and CN Bio replicate hepatic metabolism with higher fidelity than two-dimensional monocultures, reducing false-positive rates in chromosomal aberration testing by an estimated 25–30%.

Ask for Customization:

https://www.marketresearchfuture.com/ask_for_customize/32035

Market Segment Insights

BY TESTING METHODOLOGY

In Vitro Testing: Dominant segment with approximately 69.0% revenue share in 2025. Led by the Ames test genetic toxicology platform and micronucleus assays. Regulatory agencies worldwide require at least two in vitro endpoints before advancing to clinical trials. Reagent and kit innovations, such as Xenotech’s S9 metabolic activation fractions and Gentronix’s GreenScreen HC reporter assay, are improving sensitivity and reducing false-positive rates, further entrenching in vitro dominance. In vitro tests constitute the backbone of the genetic toxicology testing market because they offer faster turnaround, lower cost, and broader regulatory acceptance than in vivo alternatives.

In Silico/Computational Testing: Fastest-growing methodology segment at 9.45% CAGR (2026–2035). Fueled by AI-driven genotoxicity assessment tools and ICH M7’s endorsement of QSAR-based mutagenicity prediction for pharmaceutical impurities. Platforms incorporating deep-learning architectures trained on curated Ames test genetic toxicology databases are achieving predictive accuracies above 90%, enabling sponsors to triage thousands of impurities computationally before committing to wet-lab DNA damage testing services.

BY COMPONENT

Reagents & Consumables: Dominant segment with 42.4% share in 2025. Recurring spend on culture media, S9 fractions, staining kits, bacterial tester strains, top agar, histidine supplements, and positive-control mutagens that must be replenished per study. This non-discretionary, recurring purchase cycle underpins the segment’s majority position.

Services: Fastest-growing component segment at 9.85% CAGR (2026–2035). As sponsors increasingly outsource chromosomal aberration testing and integrated genotoxicity assessment tools packages to CROs with GLP-certified facilities. Small and mid-cap biotech companies, representing 65% of Phase I IND applications in 2024, are seeking to outsource full preclinical safety packages rather than develop internal expertise for chromosomal aberration testing.

BY APPLICATION

Pharmaceuticals & Biotechnology: Dominant application with 52.8% share in 2025. Every IND submission to the FDA, EMA, or PMDA must include results from validated mutagenicity testing assays. China’s NMPA approved a record 85 biologics license applications in 2024, each mandating Ames test genetic toxicology data and in vitro micronucleus assessment.

Cosmetics & Personal Care: USD 32.70 Million in 2025, growing rapidly. The EU prohibition of animal testing for cosmetics under Regulation (EC) 1223/2009, echoed by India, South Korea, and numerous ASEAN countries, leaves cosmetic makers with little choice but to rely on approved in vitro genotoxicity screening batteries. This category is smaller than pharmaceuticals but is growing at double-digit rates and represents an addressable potential worth an estimated USD 58 million by 2030.

BY END USER

Pharmaceutical Companies: Largest segment. Driven by IND-enabling preclinical safety packages and regulatory submission requirements. Each candidate must pass a tiered battery of DNA damage testing services before receiving first-in-human clearance.

Contract Research Organizations (CROs): Fastest-growing end-user channel. As sponsors outsource full preclinical safety packages, CROs offering integrated DNA damage tests from bacterial reverse mutation to in vitro micronucleus and computational screening can generate recurring revenue from multi-compound pipeline agreements.

Read Detailed Insights:

https://www.marketresearchfuture.com/reports/genetic-toxicology-testing-market-32035

Regional Outlook

North America — Dominant Market (~39.5% Share, USD 151.32 Million, 2025)

The United States generates approximately 81.2% of North American Genetic Toxicology Testing Market revenue, driven by the FDA’s Center for Drug Evaluation and Research pipeline throughput—over 4,800 INDs were active in 2024. The U.S. CRO ecosystem, where Charles River Laboratories and Labcorp Drug Development operate GLP-certified mutagenicity testing assays at scale, anchors regional demand.

Canada contributes through Health Canada alignment with ICH guidelines at approximately 10.8% of regional share. Mexico is growing on COFEPRIS modernisation programme at USD 12.10 Million in 2025. North America’s leadership rests on regulatory depth and the structural preclinical safety segment created by expanded FDA approvals and precision-medicine mandates.

Europe — Second Largest (~29.2% Share, 2025)

Europe’s Genetic Toxicology Testing Market reflects harmonized REACH and CLP regulations mandating comprehensive in vitro genotoxicity screening for chemicals, cosmetics, and agrochemical actives. Germany leads regionally with BfArM pharmaceutical approvals pipeline at approximately 7.85% CAGR (2026–2035). The United Kingdom contributes USD 14.50 Million on MHRA independent post-Brexit framework. France contributes approximately 16.8% of regional share through ANSM biologics emphasis. Italy contributes approximately 10.4% of regional share on cosmetics industry cluster demand.

Spain is growing at approximately 6.20% CAGR on emerging CRO hub positioning. The Nordic countries contribute USD 7.80 Million on academic-industry translational research. Russia holds approximately 4.1% of regional share through domestic pharmaceutical self-sufficiency drive. The rest of Europe contributes USD 11.30 Million on OECD mutual acceptance of data. Harmonization pressure from ECHA guidance and EU REACH revision is gradually lifting baseline demand across the region.

Asia-Pacific — Fastest-Growing Region (10.30% CAGR, 2026–2035)

Asia-Pacific is the engine of the Genetic Toxicology Testing Market. China holds the largest regional share at approximately 32.5%, with NMPA biologics registration surge—a record 85 biologics license applications approved in 2024, each mandating Ames test genetic toxicology data and in vitro micronucleus assessment. India is growing at approximately 11.45% CAGR on the back of biosimilar pipeline and contract testing exports—Indian biosimilar sponsors are responsible for roughly 40% of global biosimilar filings and are increasingly procuring domestic DNA damage testing services.

Japan contributes USD 12.90 Million through PMDA advanced therapy approvals. South Korea is growing at approximately 9.80% CAGR on K-FDA cosmetics animal-testing ban. ASEAN economies hold approximately 8.5% of regional share on pharmaceutical manufacturing FDI. The rest of Asia-Pacific contributes USD 5.20 Million on capacity building initiatives. The region’s combined biologics manufacturing expansion anchors the global volume base for genotoxicity assessment tools demand.

Middle East & Africa — Emerging Opportunity (~4.4% Share, 2025)

The Middle East & Africa carries significant opportunity. Saudi Arabia leads the region with Vision 2030 pharmaceutical localisation, contributing approximately 28.5% of regional share. The UAE is growing at approximately 7.90% CAGR on free-zone CRO investment incentives. South Africa contributes USD 3.40 Million on SAHPRA regulatory modernisation. Egypt holds approximately 14.2% of regional share as a generic pharmaceutical production hub.

The rest of MEA is growing on infrastructure development programmes at USD 3.80 Million. Saudi Arabia’s Vision 2030 has channelled SAR 8 billion into domestic pharmaceutical manufacturing, creating demand for local chromosomal aberration testing and DNA damage testing services laboratories that can support registration dossiers without relying on overseas CROs.

South America — Growing Presence (USD 23.37 Million, 2025)

Brazil anchors South America’s Genetic Toxicology Testing Market at approximately 62% of regional revenue, with ANVISA’s alignment with ICH genotoxicity guidelines and the country’s sizeable agrochemical sector requiring mutagenicity testing assays for pesticide active ingredients under Resolution RDC 294/2019, providing a stable demand floor that smooths regional forecasts. Argentina is growing at approximately 8.15% CAGR on agricultural chemicals testing demand. The rest of South America is growing on regional CRO network expansion at USD 5.10 Million in 2025.

Competitive Landscape and Recent Developments

The Genetic Toxicology Testing Market exhibits medium concentration, with an estimated top-five player share of 35–42% and a Herfindahl–Hirschman Index (HHI) below 1,000. Competition centres on GLP-certified lab capacity, proprietary genotoxicity assessment tools, and global regulatory filing support. Concentration is highest in high-income segments where regulatory and capital barriers are steep; the emerging-market tier is more fragmented as regional CROs compete on price and turnaround time.

The competitive landscape is stratified between full-spectrum global CROs offering end-to-end preclinical safety packages, specialist genotoxicity assessment tools providers with proprietary in vitro platforms, and software vendors delivering QSAR and AI-driven predictive toxicology solutions.

KEY COMPANIES AND RECENT MILESTONES

Eurofins Scientific (2024–2025): Maintains leadership with full-spectrum GLP mutagenicity testing assays including Ames, micronucleus, and comet assays across 60+ testing sites globally, commanding approximately 8–11% of global Genetic Toxicology Testing Market revenue. Global CRO scale leader with unmatched geographic footprint.

Charles River Laboratories (September 2022): Announced a collaboration with Cure AP-4 for gene therapy production. The first CDMO in North America to acquire EMA approval to commercially manufacture allogeneic cell therapy medicinal products. Estimated revenue share: approximately 7–10%. End-to-end drug development partner with integrated preclinical safety packages.

Labcorp Drug Development (2024–2025): Chromosomal aberration testing and regulatory consulting anchor a strong FDA submission track record. Estimated revenue share: approximately 6–9%.

Future Outlook: 2026–2035

By 2030, AI-autonomous genotoxicity screening pipelines will become the operating system of preclinical safety assessment. Fully automated screening workflows that integrate robotic liquid handling, high-content imaging, and AI-based mutagenicity prediction are expected to reduce end-to-end study timelines from 8 weeks to under 10 days. These closed-loop systems will redefine throughput economics in the genetic toxicology testing market and lower the per-compound cost of genotoxicity assessment tools by 50–60%. Major EHR vendors are already developing APIs for injectable device data, suggesting that connected platforms will become a reimbursement differentiator by 2030.

Platform convergence and organ-on-chip scale-up will reframe cost structures by the early 2030s. Organ-on-chip developers are pursuing multi-organ configurations that combine hepatic, renal, and bone-marrow compartments, enabling simultaneous DNA damage testing services and ADME profiling on a single device. The global microphysiological systems sector is forecast to exceed USD 400 million by 2030, with genetic toxicology applications constituting a fast-growing vertical. As per-device costs fall with scale, the addressable channel widens from centralized CROs to decentralized biotech labs and academic research centers, extending genotoxicity assessment tools beyond traditional settings.

More Related Research Insights:

https://www.marketresearchfuture.com/reports/adme-toxicology-testing-market-6945

https://www.marketresearchfuture.com/reports/in-vitro-toxicology-testing-market-21965

https://www.marketresearchfuture.com/reports/molecular-diagnostics-market-1171

https://www.marketresearchfuture.com/reports/drug-discovery-services-market-5870

https://www.marketresearchfuture.com/reports/preclinical-cro-market-7274

https://www.marketresearchfuture.com/reports/high-throughput-screening-market-1280

https://www.marketresearchfuture.com/reports/personalized-medicine-market-2937

Larry Wilson

WantStats Research And Media Pvt. Ltd.

+1 855-661-4441

email us here

Visit us on social media:

LinkedIn

Facebook

YouTube

X

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

![]()

Media gallery